Fast Business Loans: Where to Find Same-Day Approvals

In today’s fast-paced economy, fast business loans (also called instant business loans or same-day business loans) can provide critical funding for U.S. companies facing urgent expenses or opportunities.

These loans are designed to be approved and funded in 24 hours or less, much faster than traditional business financing. Fast business loans usually come in forms like short-term loans, lines of credit, merchant cash advances, or invoice financing.

In this guide, we explore what fast business loans are, how they work, and where to find them in the USA. We compare traditional bank options with online lenders, and provide a comparison table of top same-day lenders, detailing features, interest rates, and funding speed.

What Are Fast Business Loans?

A fast business loan is a small-business financing product that offers an unusually quick turnaround. By definition, same-day or instant business loans are designed to be approved and funded within 24 hours of application.

This is far faster than most bank loans; Bankrate notes that while online lenders can fund loans in as little as 24 hours, bank financing often takes days or even weeks to complete. Fast loans typically require less paperwork and can often be applied for online in minutes.

Key characteristics of fast business loans include:

- Speed: Lenders use streamlined, automated underwriting to make decisions quickly. In many cases you can get approved and funded on the same day. For example, OnDeck advertises same-day funding for loans up to $100,000 (if you apply early in the day).

BlueVine says approved applicants can access line-of-credit funds in as fast as 24 hours. And Credibly promises funds in a bank account within 24 hours of approval. - Shorter Terms: Because of the quick payout, these loans usually have shorter repayment periods. Often they must be repaid in 12 months or less, though some lenders offer up to 24 months.

- Flexible Use: The funds can be used for almost any business purpose (working capital, payroll, inventory, marketing, etc.). Same-day loans tend to be flexible, unlike traditional loans that may restrict uses.

- Higher Cost: The trade-off for speed is cost. Same-day loans generally carry higher interest rates and fees than longer-term bank loans. Lenders compensate for the risk and speed by charging premiums.

For instance, one analysis notes that fast, same-day loans often have “higher interest rates and shorter repayment periods” than traditional loans.

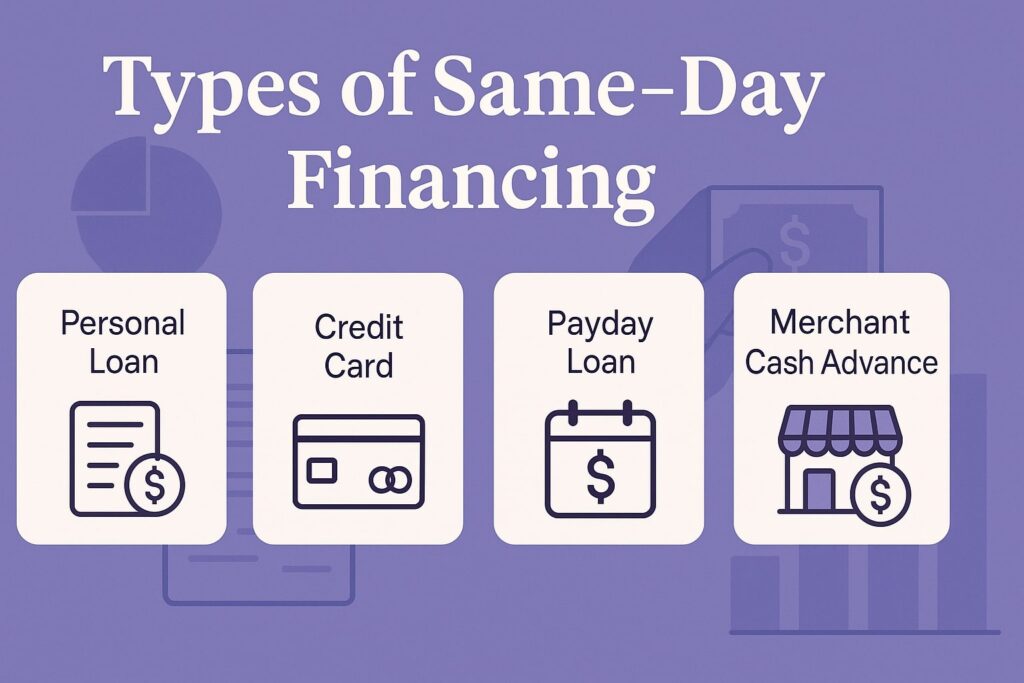

Types of Same-Day Financing

Several loan products can qualify as fast business loans. Common types include:

- Short-Term Loans: Lump-sum loans with fixed repayment schedules, but very short terms (often 3–18 months). These can be funded in a day or two.

- Business Lines of Credit: Revolving credit lines that businesses can draw on as needed. Lines of credit function like credit cards: you borrow up to a limit, repay, and borrow again.

Many fintech lenders offer lines of credit with quick approval. For example, BlueVine’s online application can give a decision in about 5 minutes, and draws can post in hours. - Merchant Cash Advances (MCAs): Not technically loans but cash advances repaid via a percentage of daily credit/debit card sales.

MCAs provide rapid funding (often next-day) because repayment is tied to sales, not a fixed schedule. They are flexible but usually very expensive, with factor rates instead of interest. - Invoice Financing (Factoring or Advance): If you have outstanding invoices, you can borrow against them. A lender or factor buys or advances up to ~90% of your invoiced amounts, often in a day or two. Invoice financing speeds cash flow without waiting 30-60 days for customers to pay.

- Equipment Loans: For buying equipment, some lenders (e.g. Triton Capital) can fund equipment loans in as little as 24 hours. These may require the equipment as collateral, which can speed approval.

Each option has different rates and eligibility, but they all share the promise of quick funding.

Traditional Banks and Credit Unions

Traditional banks and credit unions can provide business loans, but they generally do not advertise “same-day” funding. Bank loans often involve lengthy underwriting and paperwork. As Bankrate explains, even short-term business loans from a bank can take weeks to close, because banks require extensive documentation and credit checks.

However, banks have advantages too: they often offer lower interest rates, better terms (longer repayment), and support through local branches. Some banks offer business lines of credit or term loans, but they usually require stronger qualifications (higher credit scores, more time in business).

For example, Wells Fargo’s business lines of credit have competitive terms and rewards, but funding times are not guaranteed and require at least a 680 credit score. In general, if you need capital faster than a few days, online or alternative lenders are better suited to “same-day” goals.

If you prefer a bank, note that a few well-known banks have online application processes that can give quick decisions (sometimes within 24 hours), but even then the transfer of funds can take a few days.

The Small Business Administration (SBA) also guarantees many bank loans, but SBA processing is much slower (weeks to months) and not an instant option.

Credit unions similarly offer small business loans and lines of credit to members, but these too generally follow the traditional pace of application and approval.

Online Lenders and Alternative Financing

In contrast to banks, online lenders and fintech platforms specialize in speed. These lenders automate underwriting using business data (bank statements, payroll, sales, etc.) and can approve loans almost instantly. Many have minimal paperwork: often just a short online form and document upload.

For example, Lendio and Fundera are marketplaces that match borrowers with many lenders; applying through them can yield multiple offers quickly.

Specialized fintech companies like OnDeck, Kabbage (now American Express Blueprint), BlueVine, Credibly, and National Funding focus on rapid short-term loans and lines of credit. They often advertise “pre-approvals in minutes” and “funding within one day.”

- OnDeck offers both term loans and lines of credit. It can fund up to $100,000 the same business day if you apply early (by 10:30 a.m. ET), and larger loans shortly after.

OnDeck’s average APR is relatively high (around 56% in 2025), but for a portion of borrowers with excellent credit, rates can be much lower. OnDeck requires about 12 months in business and a credit score of 625+, but it is very clear about eligibility and has a fully online application. - BlueVine provides a business line of credit (up to $250k) and invoice factoring. It boasts quick approvals (as little as 5 minutes to decision) and funds can appear in your account within 24 hours of an approved draw.

BlueVine’s interest rates are relatively low for this category (starting around 7.80% APR) but you must have an established business (usually 2+ years) and ample revenue ($10K+ monthly). - Credibly connects you with its own loan products and partners. It offers working capital loans up to $600,000 and merchant cash advances. Credibly advertises “approval in as fast as 2 hours” and funds in as little as 24 hours.

Its factor rates start around 1.11 (11%). Qualification is flexible: it asks for 6+ months in business and $15K+ monthly deposits. It’s known for working with companies of marginal credit or those needing fast funding. - PayPal Working Capital is an option if you already use PayPal for your business. It’s not a traditional “loan” – you get an advance and repay via a fixed percentage of your PayPal sales.

Approved PayPal merchants can receive funds within minutes into their PayPal account. You choose a one-time fee (effectively an interest rate) before signing. Repayment happens automatically from sales, so in principle there is no fixed term or interest, just one bundled fee.

Typical fees range from about 7% to 30% of the amount borrowed (depending on repayment terms). Because funds go into your PayPal balance, withdrawals to your bank may take an extra day or two. There is no credit check – eligibility is based on PayPal sales history. - American Express Business Blueprint (formerly Kabbage) offers revolving lines of credit up to $250,000. The application is online and links to your bank account for instant approval.

Unique perk: if you use an Amex Business Checking account, draws from the line are deposited immediately into that account.

Otherwise, funds arrive as fast as same-day or next-day. The line’s interest rates depend on credit (a fee is paid as part of the loan). Typical qualification is about 1 year in business and a 660+ FICO score.

Other noteworthy lenders include National Funding, QuickBridge, Fora Financial, Triton Capital (for equipment), and financing marketplaces like Lendio.

Many of these specialize in short-term loans and equipment loans with quick turnaround. In general, any lender that advertises “quick approval” or “instant decision” likely falls into this fast-loan category.

Top Lenders for Same-Day Business Loans

Below is a comparison of several prominent fast-loan providers. It includes both fintech lenders and one alternative financing product. The table highlights each lender’s type of product, maximum loan size, interest rate (or fee), and typical funding speed.

| Lender | Type of Loan | Max Loan | Interest / Fee | Funding Speed |

|---|---|---|---|---|

| OnDeck<br/>(Term Loan) | Unsecured term loan | $5K–$250K (as low as $5K) | APR from ~35% (avg 56%) | Same business day (for loans up to $100K) |

| BlueVine<br/>(Line of Credit) | Revolving credit line | $5K–$250K | Starting ~7.8% APR | Funds in as little as 24 hours |

| Credibly<br/>(Working Capital/MCA) | Working capital loan / MCA | Up to $600K | Factor rate from 1.11 (~11%) | About 1 day (as little as 24 hours) |

| National Funding<br/>(Term Loan) | Unsecured term loan | $5K–$500K | Factor rate from 1.10 (~10%) | Same/next business day (fast funding) |

| PayPal Working Capital | Merchant cash advance | Up to ~$125K<sup>†</sup> | One-time fixed fee (approx 7–18%) | Within minutes (funds to PayPal account) |

| AmEx Business Line<sup>‡</sup> | Revolving line of credit | $2K–$250K | Varies by term (no prepay penalties) | Instant deposit to AmEx checking |

<sup>†</sup>Maximum depends on PayPal sales history (typically up to 35% of annual PayPal sales). No interest, one fixed fee paid via sales.

<sup>‡</sup>American Express Business Line of Credit (formerly Kabbage). Interest as low as ~8-18% APR; requires link to AmEx checking for instant funding.

Each lender above has features worth noting:

- OnDeck – One of the most well-known fast lenders. Offers loans up to $250K. OnDeck will actually deposit funds the same day for smaller loans (≤$100K) if you apply by mid-morning.

You need at least 12 months in business and a credit score in the mid-600s to qualify. OnDeck’s rates can be high: the average APR is around 56% (for borrowers in 2025), though the lowest-qualified borrowers can see rates in the low 30s or even 20s.

It requires a personal guarantee and a UCC lien on business assets, but has a very streamlined online process. - BlueVine – Offers an unsecured line of credit (revolving) up to $250K, and also invoice factoring. BlueVine is known for its quick approval – you can get a decision in minutes and funds within 24 hours for a draw.

Its rates are relatively low for fast financing (starting ~7.8% APR). To qualify you typically need 12–24 months in business and at least ~$480K in annual revenue.

BlueVine also provides 1.5% APY on deposits if you open a business checking account, adding to its appeal. - Credibly – Provides both term loans and merchant cash advances up to $600K. It boasts “funds in as little as 24 hours” after approval. Credibly’s factor rates start at 1.11 (≈11%).

It is flexible on credit (scores 500+ can qualify) and time in business (minimum 6 months), though it requires moderate revenue ($180K+ per year).

Borrowers can pay off early for discounts (hence its “early repayment” award by Bankrate), but overall costs can be high for lower-credit customers. - National Funding – Another online lender, National Funding offers term loans up to $500K. It advertises quick funding (“can provide funding to borrowers quickly”) and even gives a small discount for early payoff.

The minimum personal FICO is 660, and the annual revenue requirement is high ($250K). Its factor rates start at about 1.10 (≃10%), so roughly comparable to Credibly on the low end. Funding often happens the same or next day once approved. - PayPal Working Capital – This is a specialized option for U.S. businesses that process sales through PayPal. You choose an advance amount (up to a portion of your PayPal sales history) and a fixed fee up front.

There’s no credit check. If approved, PayPal funds your account within minutes. You repay automatically with a percentage of each sale until the loan plus fee is paid.

Since it’s repaid via sales, it can take days or weeks, but there are no missed payments due to this model (though a minimum quarterly payment is required).

Typical fees range roughly 7–18% of the loan amount (so a factor rate of 1.07 – 1.18), which is very competitive for instant funding. - American Express (formerly Kabbage Business Line) – An online revolving line of credit for small businesses. Borrowers can draw up to $250K if they have an existing AmEx business relationship.

The credit decisions are fast (score+account linking) and, critically, if you have an AmEx Business Checking account linked, funds are deposited instantly when you draw. Otherwise, transfers happen in one business day.

Rates vary (you pay a fee rather than traditional interest), but for well-qualified businesses they start in the single digits on a monthly fee basis. Qualification usually requires 1+ year in business and fair credit.

Note: There are many other lenders and methods (equipment financing companies, invoice factoring firms, marketplace lenders like Lendio, SBA alternatives, etc.), but the above are among the most widely used for speed.

How to Qualify for Fast Business Loans

While each lender has its own criteria, common qualifications for same-day business loans include:

- Time in Business: Most fast lenders require at least several months of operation. Online lenders often demand 6–12 months in business.

For example, Credibly asks for 6+ months, BlueVine for 12+ months, and OnDeck for 12 months. Some lenders (especially those focused on very early-stage) may fund after as little as 4 months, but those are less common. - Credit Score: Fast lenders vary widely here. Generally, online lenders have more flexible credit requirements than banks. Some will lend to businesses with personal credit scores in the 600s or even 500s.

For instance, Credibly advertises that scores as low as 500 may qualify, and Fora Financial will accept scores down to 570. However, getting the best rates and funding terms usually requires a higher score (700+). SBA loans or banks typically require 680–700+. - Revenue: Most online lenders want to see a minimum level of revenue. For example, BlueVine requires ~$10K–25K in monthly PayPal or bank deposits, OnDeck wants ~$100K+ annual revenue, and National Funding needs $250K/year.

PayPal Working Capital requires a minimum of $15–20K in annual PayPal sales. In general, expect to show 3–6 months of bank statements or processing history. - Documentation: Fast loans often require proof of business identity (EIN, bank accounts), recent bank statements or payment processor logs, and a personal credit check.

The good news is lenders typically do not ask for full business tax returns or lengthy financial projections. Many streamline the process with real-time bank account connections or simple uploads. - Collateral/Guarantees: Some short-term loans and MCAs are unsecured, but others (especially larger loans) may require a personal guarantee and/or collateral (e.g. equipment, real estate, or blanket lien).

For instance, OnDeck places a UCC lien on business assets, while PayPal Working Capital is essentially unsecured because it’s paid via sales.

Pros and Cons of Same-Day Business Loans

Obtaining a business loan on the same day has clear benefits and trade-offs:

Advantages

- Speed: The most obvious benefit is time. Same-day loans provide immediate access to capital, which can save the day if you have an urgent expense (like payroll, equipment repair, or buying a bulk inventory deal).

As one expert notes, quick funding lets businesses “swiftly address cash flow issues or growth opportunities”. - Simplicity: These loans usually involve little paperwork. Many applications take only minutes online. There’s no need to gather months of tax returns or meet with a loan officer in person.

- Flexibility: Fast loans often come with fewer restrictions on use of funds. You can generally spend the money on whatever your business needs most. This contrasts with some long-term loans that may restrict expenditures to specific purposes.

Disadvantages

- Higher Cost: You typically pay a premium for speed. Same-day loans often have much higher interest rates and fees than bank loans.

Lenders charge this to offset risk. For example, PayPal Working Capital’s fixed fees can average 15–30% of the loan, and average APRs for fintech term loans can be 30–60%. - Short Terms: These loans usually must be repaid quickly (often within a year), which can strain cash flow if the extra revenue doesn’t arrive.

- Risk of Debt Cycle: If a business relies too much on expensive short-term funding, it can lead to a cycle of debt. Financial advisors warn that these loans should be used judiciously for true emergencies or one-time opportunities.

In summary, same-day loans offer a fast lifeline when you need money yesterday, but they should be used carefully given the higher costs.

How to Apply for Fast Business Loans

To apply for a same-day loan, you generally follow these steps:

- Research Lenders: Compare options like those in the table above. Check rates, fees, and eligibility.

- Gather Documents: Even fast loans require some paperwork. Typical documents include your driver’s license, business ID (EIN), bank account statements or merchant processor statements for the last 3–6 months, and financial statements. Many lenders just need a quick bank connection or a few statement uploads.

- Fill Out Application: Most online lenders have a short application form. Expect to enter your business name, revenue, time in business, and owner information. This usually takes 10–20 minutes.

- Get a Decision: Good fintech lenders give decisions almost instantly or within a few hours. They use automated underwriting to analyze your data. You might receive conditional approval in minutes, or hear from a loan advisor.

- Review Terms: If approved, carefully review the offer. Look at the APR or factor rate, total repayable amount, term length, and any fees (origination fees, prepayment penalties, etc.). Because offers may expire, decide quickly if you want to accept it.

- Finalize and Receive Funds: Once you sign the loan agreement electronically, the lender will disburse funds. This might happen the same day (especially if you draw on a line of credit) or the next business day.

For example, OnDeck funds same-day for on-time loans, PayPal deposits within minutes, and BlueVine within 24 hours.

Be sure you have a dedicated business bank account and that any connected bank login credentials are ready. Your responsiveness can also speed up the process; quickly return any emails or calls the lender might make.

Remember that some lenders (like OnDeck or PayPal) have cut-off times (e.g. before 10:30am ET for same-day funding, or 5pm ET for next-day PayPal transfers), so time your application accordingly.

FAQs

Q: Can any small business get a same-day loan?

A: Not any business, but many can if they meet basic criteria. Lenders look for stable recent revenue (often 6–12 months of history) and reasonably good credit. Startups (under 3–4 months old) and businesses with very low revenue or poor cash flow may have trouble.

However, some lenders (like certain merchant cash advance providers or lines of credit) will consider younger businesses if sales data is strong. In general, expect to have at least half a year in business and some verifiable revenue.

Q: Do banks or credit unions offer same-day business loans?

A: Rarely. Traditional banks and credit unions typically take days or weeks to process a loan. Some banks do have quick online applications, but even if approved quickly, transferring funds can still take a few days (or longer for higher loan amounts). For true same-day funding, online lenders and fintechs are the usual source.

Q: What credit score do I need?

A: Requirements vary. Many fast lenders are more lenient than banks. You’ll often see minimum personal credit scores of 600–640 for term loans or lines.

Merchant cash advances and revenue-based options (like PayPal) may have no credit check. In any case, higher credit (700+) will yield better rates. If your score is in the 500–600 range, you may still get funded but at higher cost.

Q: How much does a same-day loan typically cost?

A: They tend to cost more than traditional loans. Interest rates (APR) for these can range from the high teens into the triple-digits in worst cases. For example, one fast lender’s average term-loan APR is ~56%.

Another financing (merchant cash advance) might cost a fixed fee of 10–30%. Always check the total payback amount. Bankrate and NerdWallet warn that same-day funds “often have higher interest rates and fees”. Use them for urgent needs, not regular financing.

Q: How fast is funding, really?

A: It depends on the lender and your banking arrangements. Many online loans are funded within 1–2 business days after approval. Some can fund on the same day: OnDeck (for loans ≤$100K by 10:30am), or PayPal (within minutes).

Lines of credit often fund fastest (draws can post within hours if bank-linked), whereas taking out a large term loan might still take a couple days to arrive in your account.

Q: Are there any hidden fees?

A: Reputable lenders will disclose all fees upfront, but read carefully. Some “fast” loans include origination fees (1–5% of loan), underwriting fees, or prepayment penalties. Pay attention to the APR or total payback.

According to a SoFi article, same-day loans “often have higher interest rates and fees”, so be sure you understand the full cost. Avoid lenders that promise quick cash but aren’t transparent about fees.

Q: What if I have bad credit?

A: Options still exist. Some short-term lenders and alternative products cater to low-credit businesses. Merchant cash advances (like PayPal) don’t require credit checks – they base approval on sales history.

Some online lenders (Credibly, Fora Financial, etc.) will consider scores in the 500s, though at higher rates. Also consider community development financial institutions (CDFIs) and microlenders in the U.S., which may offer relatively fast small loans to underserved businesses, albeit usually not literally same-day.

Conclusion

Fast business loans (instant or same-day financing) can be a vital resource for U.S. businesses needing quick cash for payroll, inventory, repairs, or unexpected opportunities. These loans are typically short-term and come with streamlined online applications, so approval and funding can often happen within 24 hours.

For example, fintech lenders like OnDeck, BlueVine, and Credibly, as well as platforms like PayPal Working Capital, advertise decision times of minutes and funding times of hours or one day.

However, borrowers should weigh the benefits against the costs. Same-day loans generally charge higher interest and fees than traditional loans, and are meant for urgent needs rather than ongoing financing.

Traditional banks and credit unions offer more affordable terms but are not suited for immediate funding needs. To pursue a fast loan, shop around with both banks (which may offer lines of credit with moderate speed) and alternative lenders (which are built for speed).

Compare offers carefully, review eligibility requirements, and be prepared with the necessary documents. The comparison table above highlights some top fast-funding options as of 2025, but always verify current terms.