How to Prepare Financial Statements for Lenders

When you apply for financing, lenders don’t just look at revenue or a credit score. They look for proof: proof you can repay, proof your cash flow is reliable, proof your business is well-managed, and proof your numbers hold up under scrutiny. That proof is delivered through financial statements for lenders.

Preparing financial statements for lenders is different from preparing reports “just for taxes” or “just for internal tracking.” Lenders evaluate risk. They want clean, consistent, timely financials that tie out, follow a logical structure, and clearly explain how your business makes money, spends money, and manages debt.

The good news: you don’t need to be a CPA to get lender-ready. You do need a process. You need accuracy, documentation, and financial storytelling that stands up to underwriting.

In this guide, you’ll learn how to prepare financial statements for lenders step-by-step, what lenders care about most, what red flags to avoid, and how to present your information in a way that increases approval odds and improves terms.

Throughout this article, the focus is on practical preparation: reconciling accounts, choosing accounting methods, assembling lender packages, and explaining fluctuations with confidence. You’ll also see future-facing trends—how underwriting is evolving and what lenders may expect next as automation and real-time data become more common.

Understanding What Lenders Mean by “Financial Statements”

Lenders use the term financial statements for lenders in a specific way. They typically expect a standard set of reports prepared consistently each period and supported by evidence.

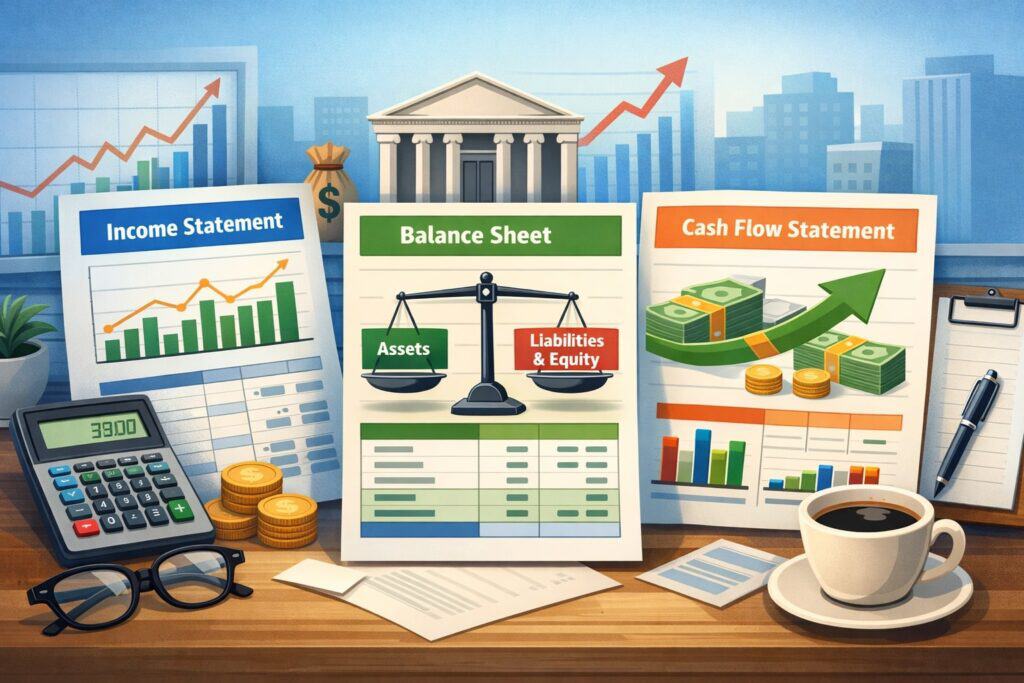

For most lenders, that standard set includes three core reports: a Profit & Loss (Income Statement), a Balance Sheet, and a Cash Flow Statement. Many lenders also request supporting schedules such as accounts receivable aging, accounts payable aging, debt schedules, and sometimes inventory summaries.

What makes financial statements for lenders different from casual financial reporting is the expectation of reliability and comparability. Reliability means your numbers match your bank activity, vendor bills, payroll, and tax filings where relevant.

Comparability means your monthly or quarterly statements use the same categories, same accounting method, and consistent classification rules. When lenders compare two periods, they want differences to reflect real operational changes—not bookkeeping inconsistencies.

Lenders also interpret financial statements using ratios and risk signals. They look for stable margins, reasonable overhead, manageable debt service, and sufficient liquidity. They want to see whether your business can handle payments even when sales dip.

That’s why preparing financial statements for lenders requires more than exporting a report from accounting software. It requires careful cleanup, correct accrual handling, and clear explanations for unusual items.

If you treat lender reporting like a professional package—not a last-minute document dump—you can reduce underwriting questions, shorten approval timelines, and often improve pricing because you look lower-risk.

The Three Core Financial Statements Lenders Expect

Profit & Loss Statement (Income Statement)

The Profit & Loss statement is often the first thing a lender reviews because it answers a direct question: does the business generate enough profit to support debt payments?

For financial statements for lenders, the Income Statement should show revenue, cost of goods sold (if applicable), gross profit, operating expenses, operating income, and net income for the requested period.

Lenders frequently ask for year-to-date figures and prior-year comparisons, and sometimes monthly detail for the last 12–24 months.

To make your financial statements for lenders stronger, present revenue and expenses in a way that reflects how you operate. If you have multiple revenue lines, break them out logically. If labor is your largest cost, show payroll categories that make sense. Avoid lumping many costs into “Miscellaneous,” which raises questions and can suggest weak financial controls.

Lenders also scrutinize profitability quality. For example, a sudden profit spike caused by a one-time insurance settlement won’t be treated like normal earnings. Clear notes and proper classification help lenders understand what is repeatable.

They may also request an EBITDA view (earnings before interest, taxes, depreciation, and amortization) because it approximates cash-generating ability.

The biggest improvement you can make is to ensure your Income Statement ties to reality: revenue matches deposit behavior, costs match vendor payments, and payroll matches filings. A clean P&L is central to lender-ready financial statements for lenders.

Balance Sheet

The Balance Sheet shows what the business owns, what it owes, and what remains as equity. For financial statements for lenders, the Balance Sheet is where underwriting digs deeper because it reveals liquidity, leverage, and working capital strength.

Lenders look at cash, receivables, inventory, fixed assets, payables, short-term debt, long-term debt, and retained earnings.

A lender-ready Balance Sheet must be accurate as of a specific date—usually month-end. That means reconciled bank balances, correct accounts receivable totals, accurate payables, and properly recorded loans.

If you have owner draws or distributions, they should be correctly reflected. If you have large “Due to/Due from” accounts or negative equity, lenders will ask for explanations.

Balance Sheet clarity matters because many loan decisions depend on it. Asset-based lenders may focus on eligible receivables and inventory. Banks may evaluate working capital and current ratios.

SBA-style underwriting may consider overall leverage and equity position. Strong financial statements for lenders minimize surprises: they show stable liquidity, reasonable liabilities, and consistent equity trends.

Cash Flow Statement

The Cash Flow Statement explains how cash actually moves through your business—separate from profitability. For financial statements for lenders, this report is crucial because debt repayment happens with cash, not accounting profits.

Lenders want to see whether operating activities generate cash consistently and whether investing or financing activities are draining it.

Many business owners skip the Cash Flow Statement because it’s less intuitive. But lenders value it because it explains mismatches: a business can show profit but still struggle to pay bills if receivables are slow or inventory is growing. A solid Cash Flow Statement demonstrates financial control and helps underwriters trust your numbers.

If your accounting system can generate a Cash Flow Statement, include it in your financial statements for lenders package. If it cannot, your lender may accept cash flow analysis through bank statements, but that usually leads to more questions and more conditions.

When you provide a clear Cash Flow Statement, you reduce lender uncertainty and improve your narrative: “Here’s exactly how operations fund debt service.”

Choosing the Right Accounting Method: Cash vs. Accrual

A major decision in preparing financial statements for lenders is whether your financials are on a cash basis or accrual basis. Cash basis recognizes revenue when cash is received and expenses when cash is paid.

Accrual recognizes revenue when earned and expenses when incurred, regardless of payment timing. Many lenders prefer accrual because it better reflects ongoing operations, especially for businesses with receivables, payables, or inventory.

If your business collects money immediately and has simple expenses, a cash basis may still work. But if you invoice clients, carry inventory, or have longer payment cycles, cash basis can distort performance.

For example, a big customer payment received in one month can make revenue look inflated, while the month you did the work looks weak. Lenders reading financial statements for lenders want to see patterns that represent true business performance.

Accrual reporting often results in better credibility with lenders because it aligns revenues and expenses to the period they belong to.

It also supports ratio analysis, margin trends, and working capital evaluation. If you present cash-basis statements, expect lenders to adjust or request accrual conversions, especially for larger loans.

A practical approach is to keep your internal books accrual and track cash flow separately. That gives you strong financial statements for lenders while still managing daily cash needs.

If you must present cash-basis statements, add supporting schedules (like AR/AP aging) and explain seasonality, large invoices, and timing differences. The goal is to remove lender uncertainty.

Step-by-Step Cleanup: Reconcile Before You Report

The fastest way to damage trust with financial statements for lenders is to submit statements that don’t tie out. Reconciliation is the foundation. Before generating your lender package, reconcile at least these areas:

- Bank accounts and credit cards

- Loan balances and interest allocations

- Accounts receivable totals and aging accuracy

- Accounts payable totals and aging accuracy

- Payroll liabilities and tax payable accounts

- Inventory counts and valuation method

- Fixed assets and depreciation (if applicable)

Start with bank reconciliation because it anchors everything. If your bank balance in accounting doesn’t match actual statements, the rest of your reports are unreliable.

Next, confirm loans: the principal balance should match lender statements, and interest expense should align with payment schedules. Then verify receivables: confirm open invoices are real, collectible, and not duplicated or stale.

For payables, ensure unpaid bills reflect actual obligations. Many businesses understate payables by paying bills directly from bank feeds without entering bills—this makes profitability look worse at random times and hides true obligations. Lenders reviewing financial statements for lenders will notice inconsistent expense timing.

Clean books also mean proper categorization. Owner draws should not be mixed into expenses. One-time costs should be labeled consistently. “Uncategorized” balances should be cleared. The cleaner your data, the fewer lender follow-ups you face. In underwriting, fewer questions often equals faster approvals and stronger terms.

Building Lender-Ready Statements: Formatting, Comparatives, and Notes

Lenders don’t just want numbers; they want readable, consistent reporting. High-quality financial statements for lenders typically include:

- A clear reporting period (month-end or year-end)

- Comparative columns (current period vs prior period; YTD vs prior YTD)

- Consistent chart of accounts categories

- Reasonable detail without excessive clutter

- Brief explanations for unusual changes

Comparatives matter because lenders evaluate trends more than single snapshots. A one-month profit doesn’t prove long-term ability to repay. A 12–24 month pattern does. If you can provide monthly P&Ls for the last year and year-end Balance Sheets for the last two years, your financial statements for lenders will look far more credible.

Include short notes where needed. Notes are not the same as excuses. They’re context. Examples: “Revenue increased due to contract renewal with Client A,” or “Gross margin declined due to supplier price changes; new pricing implemented next month.” When lenders understand the “why,” they see management competence.

Also, avoid presentation issues: messy negative signs, changing account names, or missing subtotals. Keep it professional. A lender should be able to scan your P&L and Balance Sheet and quickly understand the business model. A strong presentation is a quiet signal that your operations are disciplined.

What Lenders Look for in Financial Statements: Ratios and Signals

Lenders read financial statements for lenders through the lens of risk. They focus on repayment capacity and downside protection. While each lender is different, several core metrics appear repeatedly:

Debt Service Coverage Ratio (DSCR)

DSCR measures your ability to cover debt payments with available earnings or cash flow. Many lenders want DSCR above a minimum threshold. If your DSCR is tight, expect more documentation, a smaller loan amount, a higher rate, or additional collateral requirements.

Preparing financial statements for lenders with accurate add-backs and clear owner compensation details can materially improve DSCR presentation.

Liquidity and Working Capital

Current ratio (current assets/current liabilities) and working capital trends show whether you can handle short-term obligations. Weak liquidity triggers questions about cash management. Strong financial statements for lenders highlight stable current assets, realistic receivables, and manageable payables.

Profitability and Margin Stability

Lenders prefer stable gross margins and operating margins. If margins swing wildly, they want explanations—pricing changes, supplier shifts, seasonality, or labor changes. Your financial statements for lenders should reflect consistent classification of costs so margins are meaningful.

Leverage and Equity

Lenders evaluate total debt relative to equity or earnings. If your business is highly leveraged, lenders may still approve financing, but they will want stronger cash flow, more collateral, or personal guarantees. Accurate Balance Sheets in financial statements for lenders help you control this narrative.

The key is not to “optimize” ratios artificially. It’s to make your reporting accurate and explainable. Lenders can work with imperfect numbers if they trust them. They struggle with confusing numbers that feel unstable.

Normalizing Your Financials: Add-Backs, One-Time Items, and Owner Compensation

One of the most important lender conversations is normalized earnings. Many underwriting models adjust profit to estimate sustainable cash flow. That means your financial statements for lenders should clearly identify:

- One-time expenses (legal settlements, unusual repairs, relocation costs)

- Non-cash expenses (depreciation and amortization)

- Discretionary expenses (some owner-related items)

- Owner compensation structure (salary vs distributions)

- Extraordinary income (grants, insurance proceeds, asset sales)

Lenders often calculate an EBITDA-style cash flow and then adjust for existing debt payments to estimate repayment ability. If you have legitimate add-backs, document them. Don’t hide them inside broad categories. A clear “one-time expense” line item with a short note supports trust.

Owner compensation is especially important. If you pay yourself through payroll, it appears as an expense. If you take distributions, it appears in equity activity.

Lenders want to know whether the business can support both owner income and new debt payments. Clean financial statements for lenders separate business expenses from owner benefits.

Be careful: aggressive add-backs can backfire. Lenders may disallow them if they seem recurring or poorly documented. The best strategy is moderate, well-supported normalization that matches bank activity and invoices. This is where good bookkeeping and a simple narrative create leverage in negotiations.

Supporting Documents That Strengthen Financial Statements for Lenders

Most lenders request more than the core statements. The best loan packages include supporting schedules that validate financial statements for lenders and reduce follow-up requests.

Accounts Receivable Aging

An AR aging report shows who owes you money and how old those invoices are. Lenders care about collectability. If 40% of AR is over 90 days, they may discount it or decline. Clean financial statements for lenders include AR aging that matches the Balance Sheet receivables total, with stale invoices addressed.

Accounts Payable Aging

AP aging shows what you owe vendors. Lenders want to know if you are behind on bills. If payables are growing because you’re stretching vendors to survive, it’s a risk sign. Accurate financial statements for lenders include AP aging that ties to the Balance Sheet.

Debt Schedule

A debt schedule lists each loan, original amount, current balance, interest rate, monthly payment, maturity date, and collateral. Lenders use this to model debt service and understand lien position. If you provide a clean debt schedule alongside financial statements for lenders, you look organized and trustworthy.

Bank Statements and Interim Reports

Many lenders request the last 3–6 months of bank statements and sometimes interim financials. If your interim reports match your bank reality, underwriting goes smoother. This is a practical reason to reconcile monthly before generating financial statements for lenders.

These supporting pieces are not “extra paperwork.” They are the evidence that your reports are real.

Preparing Financial Statements for Different Loan Types

Not all financing is underwritten the same way. Tailor your financial statements for lenders package to the lender’s approach.

Term Loans and Traditional Bank Financing

These lenders often focus on DSCR, stability, and long-term viability. They prefer accrual statements, strong historical performance, and clear explanations for trends. They also want tax returns and may compare them to your Income Statement.

In this context, your financial statements for lenders should emphasize consistent profitability, stable margins, and manageable leverage.

Lines of Credit

Lines of credit often depend heavily on working capital and liquidity. Lenders may focus on receivables and inventory. Your financial statements for lenders should include strong Balance Sheet detail, accurate AR aging, and clean monthly reporting.

Asset-Based Lending

Asset-based lenders rely on collateral value (like receivables, inventory, equipment). They may discount older receivables and scrutinize concentration risk. Your financial statements for lenders need strong supporting schedules, consistent inventory valuation, and clear billing/collection processes.

SBA-Style or Government-Backed Programs

These programs can include deeper underwriting: management experience, global cash flow analysis, and more documentation. Your financial statements for lenders should be extremely consistent, with clear owner compensation details and careful reconciliation.

By aligning your package to the financing type, you reduce friction. A lender wants to quickly answer, “Can we get paid back?” Your job is to make that answer obvious.

Common Red Flags That Hurt Approval Odds

Lenders expect normal business variation, but certain issues in financial statements for lenders trigger immediate concern. Avoid these if you can, and address them directly if they exist.

One major red flag is inconsistent reporting—changing account categories every month, large “Other expense” buckets, or statements that don’t tie out.

Another is negative trends without explanation: declining revenue, shrinking gross margin, or rising overhead. Lenders may still finance you, but they will want to see a plan and proof of correction.

Cash flow strain is another common issue. Frequent overdrafts, high merchant cash advance activity, or a pattern of late payments can be visible through bank statements and liabilities. If your financial statements for lenders show growing payables and shrinking cash, lenders will ask how you’ll manage new debt.

Receivables quality matters. Large old invoices, heavy customer concentration, or frequent write-offs reduce confidence. Inventory inaccuracies also raise suspicion because they can artificially inflate assets and working capital.

Finally, commingling personal and business expenses is a credibility killer. If you want lenders to treat your business like a serious operation, your financial statements for lenders must reflect disciplined separation and clean classification. Even if the business is healthy, messy books can delay approvals or weaken terms.

Presenting Your Lender Package: How to Tell the Financial Story

Strong financial statements for lenders are not just accurate; they are communicated well. Underwriting is part math and part trust. You can build trust by presenting a clean package and a short narrative summary.

Include a brief cover note that explains: what you’re requesting, how you’ll use funds, and how repayment will be supported. Then summarize key trends: revenue growth, margin stability, cost controls, and any major changes. If there was a tough quarter, explain it and show evidence of recovery.

Your narrative should match the numbers. If you claim sales are growing but the P&L shows flat revenue, underwriting trust drops. If you claim expenses are under control but overhead categories are rising, it raises questions.

The best approach is straightforward: show what’s going well, show what changed, and show what you’re doing about it.

Also, ensure your financial statements for lenders are delivered in a consistent format—typically PDF exports from your accounting system—along with supporting schedules. Avoid screenshots and avoid editing numbers in spreadsheets without clear support. Lenders prefer “system-generated” reports because they are harder to manipulate.

When you present like a professional, lenders respond like you’re lower risk.

Using a Bookkeeper or CPA: When It’s Worth It

You can prepare financial statements for lenders on your own, but there are times when professional help is worth the cost. If your loan request is large, if you have multiple entities, if inventory accounting is complex, or if your books are behind, a qualified bookkeeper or CPA can save you time and improve outcomes.

A bookkeeper can reconcile accounts, clean up categorization, and produce consistent monthly statements. A CPA can provide higher-level assurance, help with accrual conversions, and sometimes prepare compiled or reviewed financial statements if a lender requests them.

Not every lender requires CPA-prepared statements, but higher-quality reporting can still strengthen your position.

Professional support also helps with normalization. If you need add-backs, owner compensation adjustments, or one-time expense classification, a CPA can document these in a way lenders trust. That trust can translate into better rates, fewer conditions, and faster approvals.

Even if you don’t use a professional full-time, consider a pre-application financial review. Think of it as underwriting preparation. Improving financial statements for lenders before submission is far easier than defending messy numbers after the lender flags issues.

“Latest” Lending Expectations and Future Predictions

Lender expectations continue to evolve. Even though the core of financial statements for lenders remains the same, underwriting processes are increasingly shaped by automation, data connectivity, and faster decision cycles.

One trend is the growing use of direct data connections—bank data feeds, accounting integrations, and payment processing analytics.

Lenders may request read-only access to accounting systems or bank transaction history to validate financial statements more quickly. In the near future, lenders may rely less on static PDFs and more on continuous financial monitoring, especially for lines of credit and working capital products.

Another shift is stronger attention to cash flow quality. Rather than relying only on net income, lenders increasingly model cash conversion cycles, receivable collection speed, expense volatility, and customer concentration.

This makes financial statements for lenders with accurate AR aging and consistent categorization even more important.

You may also see more standardized reporting requirements for small businesses: consistent month-end close timing, clearer owner compensation reporting, and more scrutiny on add-backs.

Businesses that close books monthly and maintain lender-ready reporting will have an advantage—faster approvals and better pricing because the lender’s verification cost is lower.

The future likely rewards financial discipline. The better your real-time data hygiene, the stronger your borrowing options.

FAQs

Q.1: What period of financial statements for lenders do I usually need?

Answer: Most lenders ask for at least the last two years of annual financials and year-to-date statements. Many also want monthly statements for the last 12 months to evaluate trends and seasonality. The stronger and more consistent your financial statements for lenders, the easier it is to support a larger request.

Q.2: Do financial statements for lenders have to match tax returns exactly?

Answer: They should generally be consistent, but differences can happen due to timing, accounting method, and tax adjustments. Lenders often compare tax filings to your financial statements for lenders to confirm revenue and profitability. If there are differences, provide clear explanations and consistent accounting support.

Q.3: Can I submit cash-basis financial statements for lenders?

Answer: Sometimes, yes—especially for smaller loans or simpler businesses. But many lenders prefer accrual because it reflects true performance. If you use cash basis, strengthen your financial statements for lenders with AR/AP aging schedules and clear notes about timing differences.

Q.4: What if my books are behind and I need financial statements for lenders quickly?

Answer: Prioritize reconciliation of bank accounts, loans, and receivables, then generate a clean month-end close for the most recent periods. Lenders prefer accurate statements over fast but unreliable ones. If needed, hire bookkeeping help to catch up and produce lender-ready financial statements for lenders.

Q.5: What are the biggest mistakes people make with financial statements for lenders?

Answer: Common mistakes include unreconciled accounts, excessive “miscellaneous” expenses, mixing personal transactions, missing supporting schedules, and inconsistent reporting periods. These issues reduce trust and increase lender conditions. Clean, consistent financial statements for lenders reduce questions.

Q.6: Do lenders require a Cash Flow Statement?

Answer: Not always, but many do—especially for larger requests. Even if it’s not requested, including it can strengthen your package. Since repayment is cash-based, Cash Flow reporting improves the credibility of financial statements for lenders.

Q.7: How can I improve my approval odds using financial statements for lenders?

Answer: Close books monthly, reconcile accounts, document one-time items, provide AR/AP aging and a debt schedule, and include clear explanations for changes. Your goal is to make underwriting simple. Strong financial statements for lenders reduce uncertainty—and uncertainty is what lenders price and restrict.

Conclusion

Preparing financial statements for lenders is one of the most powerful ways to improve financing outcomes. When your reports are accurate, consistent, reconciled, and supported by schedules, you don’t just “apply”—you present a clear credit case.

That can lead to faster approvals, fewer conditions, and stronger terms because lenders can verify performance with confidence.

The core process is straightforward: choose a consistent accounting method, reconcile accounts monthly, generate professional P&L, Balance Sheet, and Cash Flow reporting, and attach supporting documents like AR aging, AP aging, and a debt schedule. Then add a short narrative that explains trends and unusual items without defensiveness.

The businesses that win financing more easily are usually not the ones with perfect numbers—they’re the ones with trustworthy numbers. And as underwriting continues to modernize through data integrations and faster decisioning, disciplined reporting will matter even more.

If you build a repeatable month-end close process now, your financial statements for lenders will stay ready—not only for this loan request, but for future growth opportunities, better credit lines, and stronger negotiating power.