How to Improve Your Business Credit Score Quickly

Building a strong business credit score is crucial for any U.S. company – whether you run a small LLC, a new startup, a corporation, or a sole proprietorship.

A healthy business credit score (often on a 0–100 scale) is a key indicator to lenders, suppliers, insurers, and partners of your company’s financial reputation.

Indeed, poor credit is a leading reason small business loans are denied. In contrast, a good business credit score (generally around 80+ on common scales) can unlock lower interest rates, higher credit lines, and more favorable terms.

This comprehensive guide explains what affects your business credit score and lays out practical, step-by-step strategies—such as registering with credit bureaus, applying for vendor accounts, and monitoring your credit—to improve it quickly.

Business credit scores operate on scales similar to personal credit scores (often 0–100) and are based on company payment history, outstanding debt, and credit use.

An infographic above highlights key strategies: pay bills early, keep balances low, use multiple credit accounts, and monitor your credit report. Each of these factors plays a role in boosting your score and signaling reliability to lenders.

Understanding Business Credit Scores

A business credit score is a numeric summary of your company’s creditworthiness. Most major business credit scoring models (such as Dun & Bradstreet’s PAYDEX or Experian’s Intelliscore) use a 0–100 range, where higher is better.

In practice, a score of 80 or higher is considered good, indicating reliable payment performance. The score reflects factors like payment history, total debt, credit utilization ratio, business size, and public records (e.g. liens or bankruptcies).

Lenders and suppliers review your score when you seek loans, credit terms, or partnerships – so having a strong score opens doors. As one SBA study notes, about 20% of small business loan applications are denied due to unsatisfactory business credit.

Business vs. Personal Credit

Business credit is reported and scored separately from personal credit, though they share underlying principles. Personal credit uses identifiers like your Social Security number and is reported by Equifax, Experian and TransUnion.

Business credit uses your Employer Identification Number (EIN), D-U-N-S number, or business tax ID, and is reported by agencies like Dun & Bradstreet, Equifax Business, Experian Business (and sometimes FICO’s SBSS for SBA loans).

Unlike personal credit, U.S. businesses don’t get free annual credit reports by law. You must actively request or subscribe to each bureau (D&B, Experian, Equifax) if you want your business report.

| Aspect | Personal Credit | Business Credit |

|---|---|---|

| Score Range | 300–850 (FICO/Vantage) | Typically 0–100 |

| Major Credit Bureaus | Equifax, Experian, TransUnion | Dun & Bradstreet; Equifax (Business); Experian (Business) |

| Free Annual Reports | Required by law (AnnualCreditReport.com) | Not required free; business reports generally cost money |

| Key Identifiers | Name, SSN, Address | Business name, EIN, D-U-N-S, business address |

| Score Factors | Payment history, debt, credit mix, inquiries | Payment history, utilization, trade lines, longevity, public records |

What is a good business credit score?

Generally, a business credit score in the 80s or higher (on the 0–100 scale) is considered strong. For example, Dun & Bradstreet’s PAYDEX uses 1–100: scores of 80–100 indicate low risk (on-time or early payments). Equifax and Experian business scores similarly consider 80+ as excellent.

(By contrast, personal FICO scores consider 700+ as good; business scores have lower numbers since they start at zero.) The U.S. Chamber of Commerce notes that lenders often view 76+ (Experian/Equifax) or 80+ (D&B) as healthy.

If your score is below these thresholds, it’s a signal to improve payment practices, add credit references, and correct any report errors.

Why Business Credit Scores Matter

A strong business credit score yields concrete benefits for all company types (small business, LLC, startup, or corporation):

- Better Financing Terms: High scores help secure loans, lines of credit, and business credit cards more easily. Businesses with good credit typically qualify for larger credit limits, lower interest rates, and longer repayment terms.

For example, SBA 7(a) loans and bank loans often require minimum credit benchmarks, and exceeding them can speed up approval. - Lower Costs: Insurers and landlords often check business credit. A good score can lower business insurance premiums and help negotiate favorable lease or vendor contract terms. Vendors extend longer “days to pay” invoices to reliable businesses, improving cash flow.

- Supplier Trust: Suppliers and partners prefer working with businesses that have established credit histories. A strong credit profile signals stability and trustworthiness. It can even be a requirement; many vendors won’t offer net-30 terms to unincorporated or credit-new businesses.

- Risk Protection & Separation: Incorporating as an LLC or corporation provides personal liability protection, and building business credit allows you to fund the company independently of your personal finances.

This separation simplifies taxes and bookkeeping and ensures your personal credit rating remains distinct (except where personal guarantees are used).

In short, a high good business credit score positions your company for growth, resilience and better deals. According to a U.S. Chamber study, maintaining solid business credit can increase your chances of securing favorable loan terms and is crucial when lenders or partners “check your business credit score”.

Steps to Boost Your Business Credit Score Quickly

Improving a business credit score is a process, but by taking the right steps, you can see progress in a matter of months. Here is a concise, step-by-step guide to build and improve your business credit:

- Register and Structure Your Business Properly. Formally register your business as an LLC, S-Corp, C-Corp, or similar entity with your state. Choosing a legal structure separates personal and business obligations, which is crucial for credit building.

For example, Sole Proprietors have no separate business credit, whereas an LLC or corporation can establish its own EIN and credit file. Also obtain any required business licenses or permits.

Consistently use your official business name, address, and phone number on all accounts. These foundational steps make your business “real” in the eyes of bureaus and vendors. - Obtain an EIN and D-U-N-S Number. Apply for an EIN (Employer Identification Number) from the IRS (this is free and immediate online).

The EIN is like your business’s Social Security Number and is typically required to open business bank accounts and credit lines without using your SSN. Also register for a D-U-N-S Number from Dun & Bradstreet (free).

A D-U-N-S number is widely used as your business identifier by creditors; having one allows suppliers and lenders to report your payments to D&B, which builds your PAYDEX credit profile. - Open a Dedicated Business Bank Account. Keep personal and business finances completely separate. Open a business checking account under your business name and EIN. This creates a clear financial trail.

Use this account for all business income and expenses – never commingle with personal funds. Bureaus and lenders view a positive bank account history (balances, low fees) as part of creditworthiness. Some fintechs offer no-fee business accounts that include basic credit monitoring, which can be helpful. - Apply for Business Credit Accounts. The next step is to establish credit lines in your company’s name that will report to business credit bureaus:

- Business Credit Cards: Apply for one or more business credit cards using your EIN (and usually a personal guarantee).

Even if you must qualify on your personal credit now, choose cards that report to Dun & Bradstreet, Experian Business, or Equifax Business.

Use these cards for routine expenses and pay the full balance or at least well below the limit each month. Keep utilization under ~30% to help boost your score. - Vendor (Trade) Credit Accounts: Open net-30 or net-60 accounts with suppliers that report to credit bureaus. Common examples include office supply or equipment vendors.

Companies like Grainger, Quill, Uline, Home Depot, and Staples often extend 30-day terms to businesses and report those payments.

To open these, you typically provide your business information, D-U-N-S, EIN, business address, and sometimes a small first purchase. Each on-time invoice payment adds a trade line to your credit file, demonstrating reliability.

(Even if a vendor doesn’t report, you can submit the business and contact details of vendors you pay and the bureaus may use them as trade references.) - Loans or Lines of Credit: If needed and available, taking out a small business line of credit or SBA microloan and paying it diligently is another tradeline that can boost credit. However, ensure any debt is manageable; the simplest wins often come from cards and net-30 accounts for quick scoring.

- Business Credit Cards: Apply for one or more business credit cards using your EIN (and usually a personal guarantee).

- Pay All Bills On Time (Or Early). Payment history is by far the most important factor in business credit scoring. Always make payments by the due date – early payments are even better.

Business credit bureaus report how many days a payment was past due (even 2 days late counts). According to Dun & Bradstreet’s PAYDEX system, paying exactly on time results in a score of 80, whereas paying early (before due) yields scores above 90.

Even one late payment can dent your score. Use auto-pay, calendar reminders, or accounting software to avoid late invoices. Consistent, on-time payments across all trade lines and credit accounts will steadily raise your score. - Keep Balances Low (Manage Credit Utilization). Try to use only a small portion of your available credit. A healthy credit utilization ratio is generally below 30% (i.e., never charge close to your limit).

For instance, if your business credit card has a $20,000 limit, try to keep the outstanding balance under $6,000 before paying it off. Low utilization shows lenders you aren’t maxing out credit and helps improve your score.

If utilization is high, pay down balances aggressively or request a higher limit (which lowers your ratio). Over time, as your credit builds, you can responsibly increase usage knowing it won’t harm your credit. - Add Trade References (Optional). If you have significant vendor relationships, ensure they report to the bureaus. Fundbox notes that trade references (vendors and suppliers reporting payment data) are used by business bureaus to gauge payment habits.

Ask key vendors if they report your payments to D&B, Equifax, or Experian. If they don’t, most credit bureaus allow you to list trade references (names of vendors) on your account, and the bureau will contact the vendor to verify your payment history.

Consistent on-time payments to suppliers (like utility companies, office suppliers, or manufacturers) then become positive trade references that boost your score. - Monitor Your Business Credit Reports Regularly. Just like personal credit, mistakes or fraud can hurt your score. Obtain your business credit reports from Dun & Bradstreet, Equifax Business, and Experian Business at least once a year (or more often if possible).

Review them for errors, outdated information, or unexpected negatives (like a missed payment). If you spot inaccuracies, file a dispute with the reporting bureau to correct it promptly.

Regular monitoring also lets you see the results of your improvements – you should see new tradelines and score changes over time.

Services like Nav or CreditSafe offer dashboards that pull info from multiple agencies, which can simplify regular checks (although comprehensive reports usually cost money). - Maintain Good Personal Credit (When Starting Out). In the initial stages, many lenders and card issuers will look at the owner’s personal credit.

While the goal is to separate business credit, until enough business credit history exists, your personal FICO score may still impact approvals. Thus, keep your personal credit healthy (low balances, on-time payments) during the early months of your business.

As one expert notes, “your personal credit score can impact your business credit, especially if you are a new venture”. Once your business credit is established, you can lean more on EIN-based credit products.

Business Types and Credit Building

- Small Businesses & Startups: These enterprises often start with little credit history. Following all the steps above is essential: incorporate (LLC or corporation), obtain an EIN, and open multiple vendor accounts.

Early on, owners should expect to use personal credit guarantees but should work quickly to build business tradelines. Even a few on-time net-30 accounts (e.g. office supplies, utilities) can create a credit profile. - LLCs and Corporations: These already have separate legal status, which is ideal. Ensure that all business names and EINs are listed correctly with credit agencies.

Larger or older corporations may already have some tradelines; focus on expanding them (more credit cards or vendor accounts) and optimizing usage. - High-Growth Startups or Tech Companies: In some cases (especially if VC-backed), alternatives like credit-builder services (e.g. Brex) that don’t require personal guarantees can speed up credit profile building. But even then, the core principles (on-time payments, multiple accounts) remain.

- Sole Proprietors: While not directly asked, note that sole proprietors without an LLC operate under personal credit. If possible, it’s advisable to form an LLC or corporation quickly to unlock business credit options.

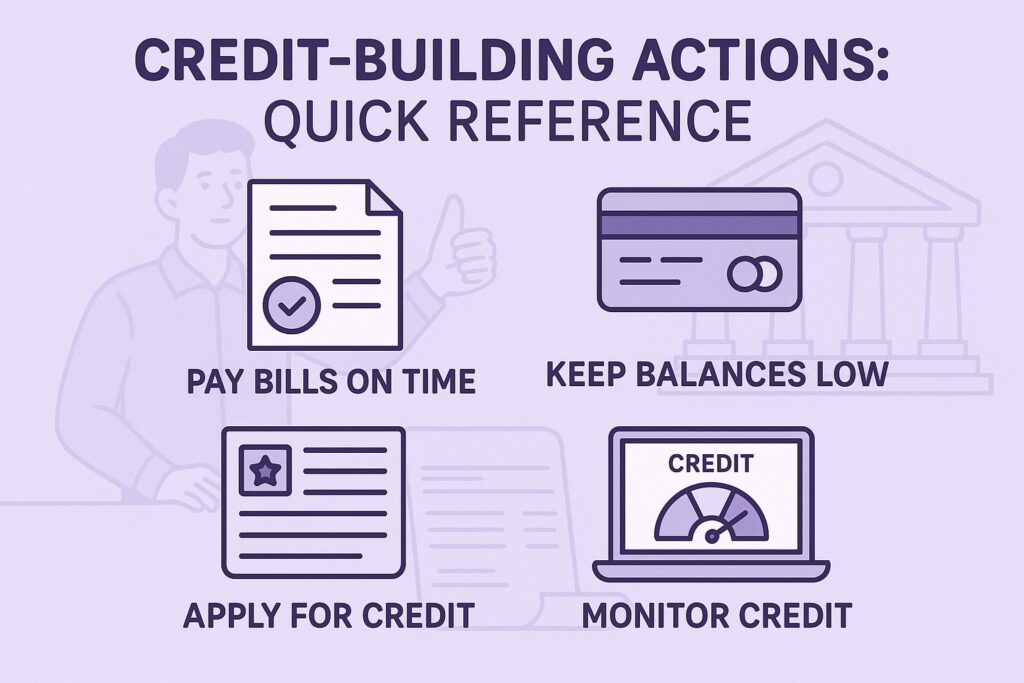

Credit-Building Actions: Quick Reference

Here are key actions summarized in a bullet list for easy reference:

- Legal and Financial Foundation: Form a legal entity (LLC, Corp), register with the Secretary of State, and obtain an EIN. Get a physical business address and phone number, and keep these consistent in all records.

- Credit Accounts: Open a business checking account and make it your primary account for all business transactions. Apply for business credit cards (ideally reporting to all three bureaus) and a few net-30 vendor accounts from suppliers that report payments.

- Reporting and Monitoring: Register your business with Dun & Bradstreet (get a D-U-N-S number) and ensure you are listed with Experian Business and Equifax Business. Regularly check your business credit reports and dispute any errors.

- Payment Practices: Make all payments (loans, leases, utilities, credit accounts) on time or early. Use autopay and reminders to avoid late payments.

- Debt Management: Keep credit utilization low by not maxing out cards or credit lines. Pay down balances before billing cycles end, or request higher limits if needed.

- Credit Diversity: Over time, add more tradelines (credit cards, lines of credit, vendor accounts). A mix of financial accounts (cards/loans) and supplier accounts builds a robust profile.

- Personal Credit (Interim): Maintain a good personal credit score to help secure initial financing. Eventually, transition to using only your EIN with corporate cards to isolate personal and business credit.

- Patience and Consistency: Building strong business credit takes several months of good habits. Consistency is key – positive actions compound over time.

Below is a comparison of Personal vs Business credit, highlighting the differences important to businesses in the U.S.:

| Metric | Personal Credit | Business Credit |

|---|---|---|

| Score Range | 300–850 (FICO/Vantage) | Typically 0–100 (e.g. D&B PAYDEX, Experian Intelliscore) |

| Major Bureaus | Equifax, Experian, TransUnion | Dun & Bradstreet, Equifax (Business), Experian (Business) |

| Free Reports | Yes (AnnualCreditReport.gov) | No – business reports must be purchased (though some services give summaries) |

| Identifiers | Name, SSN, DOB, Address | Business name, EIN, D-U-N-S, business address |

| Key Factors | Payment history, credit utilization, age of accounts, new credit | Business payment history, outstanding balances, trade lines, public records |

Common Mistakes to Avoid

- Mixing Personal and Business Finances: Using a personal credit card for business expenses (or vice versa) can blur lines and may inadvertently allow business spending to affect personal credit utilization. Keep finances strictly separate.

- Applying for Too Many Accounts at Once: Each credit inquiry can ding your personal score and overwhelm a new credit profile. Space out applications and focus on ones that report.

- Ignoring Bureaus: Some small vendors don’t report transactions automatically. Don’t assume all good behavior is captured – proactively register your business with the bureaus and update information.

- Late or Partial Payments: Making minimum payments or paying late – even by a few days – can downgrade your score. Never rely on “just paying something” – always meet full terms on-time.

- Not Checking Reports: Without regular checks, incorrect delinquencies or identity mix-ups can go unnoticed. Errors can drag down your score until fixed.

Frequently Asked Questions

Q: What is considered a good business credit score?

Answer: A strong business credit score is typically around 80 or above on the common 0–100 scales. For example, D&B’s PAYDEX score considers 80–100 as low risk. Equifax and Experian business scores also view 80+ as excellent. Scores below 50–60 may be seen as high risk. It’s best to target the 80s or 90s to unlock top credit benefits.

Q: How long will it take to improve my business credit?

Answer: Building credit is a marathon, not a sprint. You may see initial tradelines appear in a few weeks to months after opening accounts. However, establishing a good score generally takes several months of on-time payments.

For instance, new accounts must first report to bureaus (often within 30–60 days), and then you typically need at least 3–6 months of clean payment history to reach a solid score.

A Harvard study notes it can take 30–60 days for accounts to appear, and a few months of consistent payments to build a strong profile. The key is to start early and be consistent; with disciplined action, many small businesses see noticeable improvement within 3–6 months.

Q: How often should I check my business credit report?

Answer: Regularly reviewing your reports is crucial. There’s no free annual report as with personal credit, but business owners should ideally check each bureau’s report at least once a year, and more frequently if you’re rapidly building credit or planning a loan application.

Checking quarterly or semi-annually helps you spot and fix errors fast. As Pipe notes, monitoring scores helps you track progress and identify improvement areas.

Consider using paid services or services like Nav, which aggregate scores, to monitor changes. Always immediately dispute any inaccuracies, as a mistaken delinquency or duplicated debt could hurt your score.

Q: Does my personal credit affect my business credit?

Answer: Initially, yes – especially for new businesses. Most small-business credit cards and loans require a personal guarantee, meaning issuers look at your personal credit during underwriting.

If your business has little credit history, lenders may rely on your personal score and history. Therefore, it’s important to maintain good personal credit (timely payments, low utilization) early on.

Over time, as your business credit profile grows and you shift to EIN-only accounts, the business credit becomes more independent. In short, personal credit can help you start building business credit, but strong business credit ultimately stands on its own.

Q: How do vendor (trade) credit accounts help my business credit?

Answer: Vendor credit (net-30 or net-60 accounts with suppliers) is one of the fastest ways to build business credit. When vendors report your timely payments to credit bureaus, each invoice paid on time becomes a positive entry on your business credit report.

Even a few vendor accounts can establish a tradeline that gives you a business credit score. Tipalti and Nav both emphasize opening net-30 accounts with office supplies, shipping, or equipment vendors.

For example, office supply vendors like Uline, Quill, Grainger or shipping companies will often approve new businesses. Pay these accounts in full each cycle (or a day or two early) to rack up positive “Days Beyond Terms” (DBT) scores.

Positive trade references make your business appear reliable and directly boost your score. If a vendor doesn’t report by default, ask them to or add them as a trade reference on your accounts to ensure the bureau contacts them for payment verification.

Q: Can I use my personal credit card for business purchases?

Answer: It’s best to use business credit cards to build business credit. Using a personal card for business expenses doesn’t help establish a business credit history, because personal card activity typically does not report to business credit bureaus.

It also risks commingling finances. If you must start somewhere, open a business credit card (even if initially underwritten via your personal credit) and use it exclusively for business. This way, payments on the card help build the business’s credit file.

Eventually, aim to use EIN-only or corporate cards that don’t involve personal reporting to keep personal and business credit streams separate.

Q: What if I have bad credit history or late payments?

Answer: Don’t panic. A low business credit score can be improved with time and discipline. Begin by checking your reports for any errors or outdated delinquencies and disputing them if needed.

Then focus on the fundamentals: bring accounts current, pay future bills early, and add new tradelines with good terms. Over time, recent positive history will outweigh past negatives.

Analysts agree: “Making on-time payments, establishing trade lines with suppliers, and working with creditors that report to the main business bureaus are good places to start” to reverse a bad score. Consistency is key – improve habits month after month, and your score will follow.

Q: Are there services that help build business credit?

Answer: Yes, some fintech platforms (like Nav, Brex, Fundbox) offer tools or cards that report to business bureaus and track your credit profile. These can simplify monitoring and sometimes extend credit to early-stage businesses.

However, be cautious: no service can substitute for the core actions above. Use them as supplements, not replacements. The real work is in maintaining payments and multiple tradelines.

Even with such services, you still should register your business, get an EIN/DUNS, and make the traditional steps listed above.

Q: Can I build business credit if I’m a sole proprietor or freelancer?

Answer: As a sole proprietor, your business credit history is tied to your personal identity, so building a separate business credit file is more difficult. The recommended approach is to form an LLC or corporation (even a single-member LLC) to start a distinct credit profile.

Once incorporated, follow the same steps: open an EIN-based bank account, get tradelines in the LLC’s name, and monitor the new business credit scores.

Conclusion

Improving your business credit score quickly requires a systematic approach: start by establishing a solid legal and financial foundation (LLC/corp, EIN, bank account) and then open credit accounts that report to the major bureaus.

Pay all bills on time, keep credit balances low, and expand your credit relationships (cards and vendor lines) steadily. Over several months of disciplined behavior, you’ll see your score climb.

A strong business credit score (typically 80+) unlocks significant advantages: easier access to loans, better rates, more generous supplier terms, and a clear separation from personal finances.

In short, building business credit is an investment in your company’s future. By following the steps above – incorporating, obtaining an EIN and DUNS number, setting up tradelines, and monitoring your reports – you can improve your business credit score and secure better financial footing for your small business, startup, or corporation.